Connecting the Innovators

in Corporate Banking

INSPIRE:2024

Here we go again: our annual INSPIRE corporate banking event will take place on 22 May 2024 as we gather once again in the vibrant city of Düsseldorf for a day of innovation and networking.

We are looking forward to see you there and to shift the boundaries of digital corporate banking yet again.

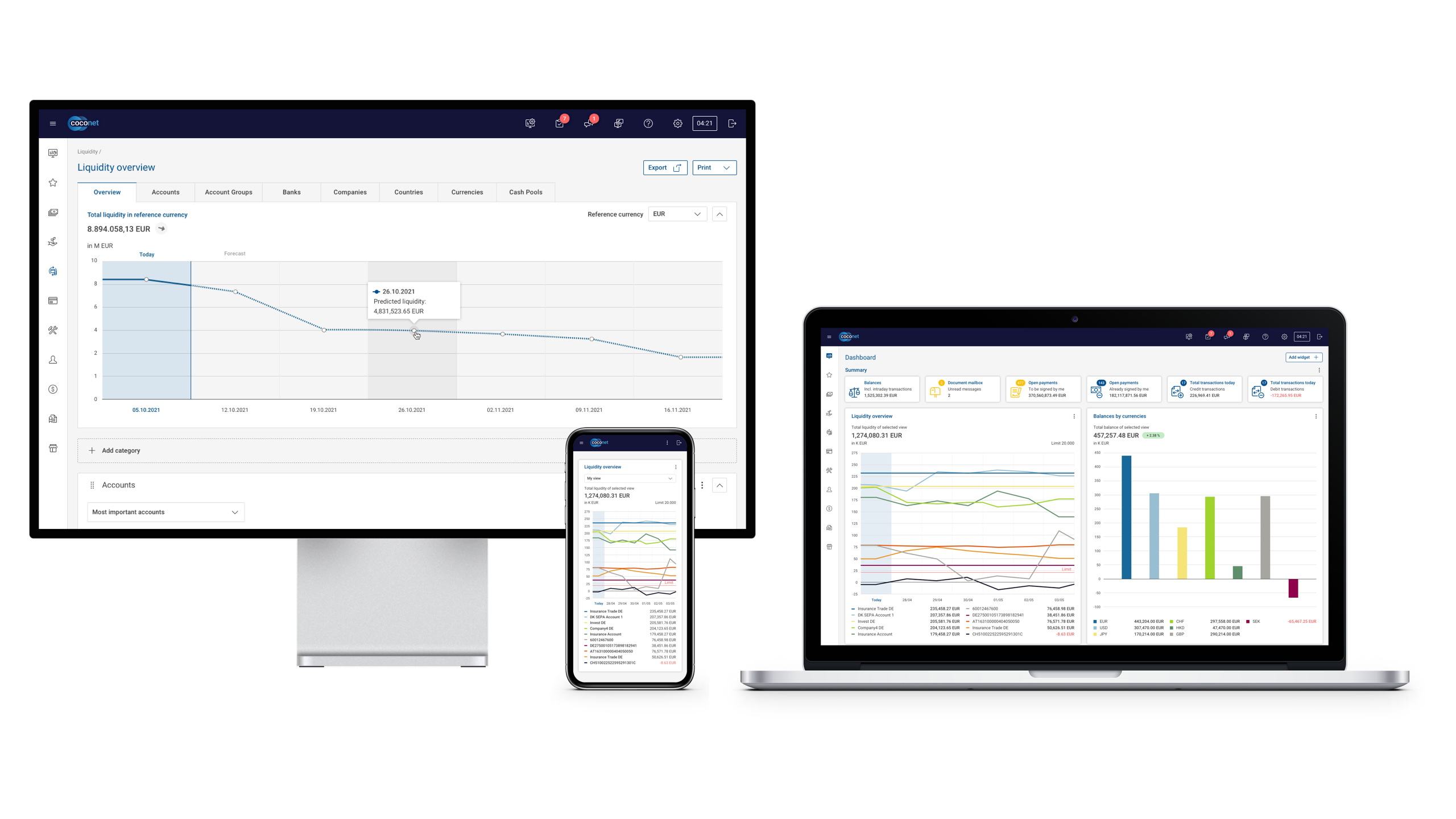

coconet accelerates banks – with the #1 whitelabelled digital corporate banking platform built by technology leaders, functional innovators and regulatory experts.

coconet group is one of Europe’s most innovative and experienced fintechs. Founded in 1984 and headquartered in Düsseldorf, Germany, coconet delivers multi:versa, a unique channel platform for corporate banking.

![[[Translate to "English"]]](/fileadmin/public/_processed_/3/7/csm_csm_headerbanner_coco_customer_news-01_9ad6e1026c.png "Press releases")

The digital channel between bank and corporate customer is our universe. And all our solutions are connected to payments. You will get products in cash management, client onboarding, digital credit processes and more right out of the box ready for corporates.

While our competitors try to cover all segments of the bank at the same time, we believe in the specifics of the corporate and business banking segment.

multi:bank is the transaction and cash management product in multi:versa. Your corporate clients’ central access channel to everyday transactions, reporting, liquidity management and much more.

Become the focal point for your corporate clients!

multi:hub is the central eBanking server within your architecture. The product connects many of our customers' various client access channels with your backend systems.

Your administrators will love multi:hub – and your clients will be impressed by its speed.

Bring your clients on board even more quickly with our product multi:onboard. The fully digital onboarding workflow, including user interaction and KYC, creates a new gateway into your bank’s environment.

Start tomorrow into the age of paperless onboarding!

multi:engage is our all-rounder product in client-bank relations. Based on this modular approach, you will benefit from numerous individual features, starting with 1:1 or group chats to document exchange with qualified digital signatures. Integrated co-browsing and a video chat channel complement the solution.

Rely on multi:engage so the touchpoint to your corporate clients becomes future-proof!

The Swiss Raiffeisen Group uses multi:bank in combination with coco:EBICS. Corporate clients are therefore provided with increased convenience based on integrated cash management in a multi-bank portal.

The Berenberg Corporate Portal is based on several multi:versa platform modules and, in addition to transactions and cash management for corporate clients, makes processes in client-bank relations easier, such as credit portfolio display, onboarding and document exchange.

Based on multi:bank, KBC offers the product “KBC Reach” to its corporate clients. They can manage their international business accounts from a central point, make payments and see all account transactions at a glance.

The LBBW ZV App in the LBBW Corporates Portal allows corporate clients access to all account information and enables them to make payments cost-effectively, securely and easily. This solution is based on multi:bank and multi:hub together with coco:EBICS.

The new cash management solution offers all PostFinance corporate clients – from mid-sized companies to international corporations – numerous features for high-performance cash management, and is based on multi:bank in combination with coco:EBICS.

The new digital banking platform for all target markets and client segments is based on multi:versa, and is an essential element of the bank’s comprehensive transformation as part of its digitisation.

With a new digital multi-banking platform, the corporate clients of Bank für Sozialwirtschaft are provided with a user-friendly overview of their accounts, bank details and transactions. BfS uses multi:hub and multi:bank for this.